There are broadly two macroeconomic stabilisation policies available to a nation: fiscal policy and monetary policy. Both emerged as central tools of economic management in response to the Great Depression of the 1930s. Prior to this period, most nations followed the doctrine of laissez-faire free markets and free trade believing in the supremacy of market forces and minimal government intervention.

The Great Depression proved to be a cataclysmic crisis for capitalism, exposing the limitations of non-interventionist policies. It was the venerable economist John Maynard Keynes who rescued capitalism through his bold ideas, articulated in his landmark work The General Theory of Employment, Interest and Money. Keynes emphasised the crucial role of government intervention when markets fail.

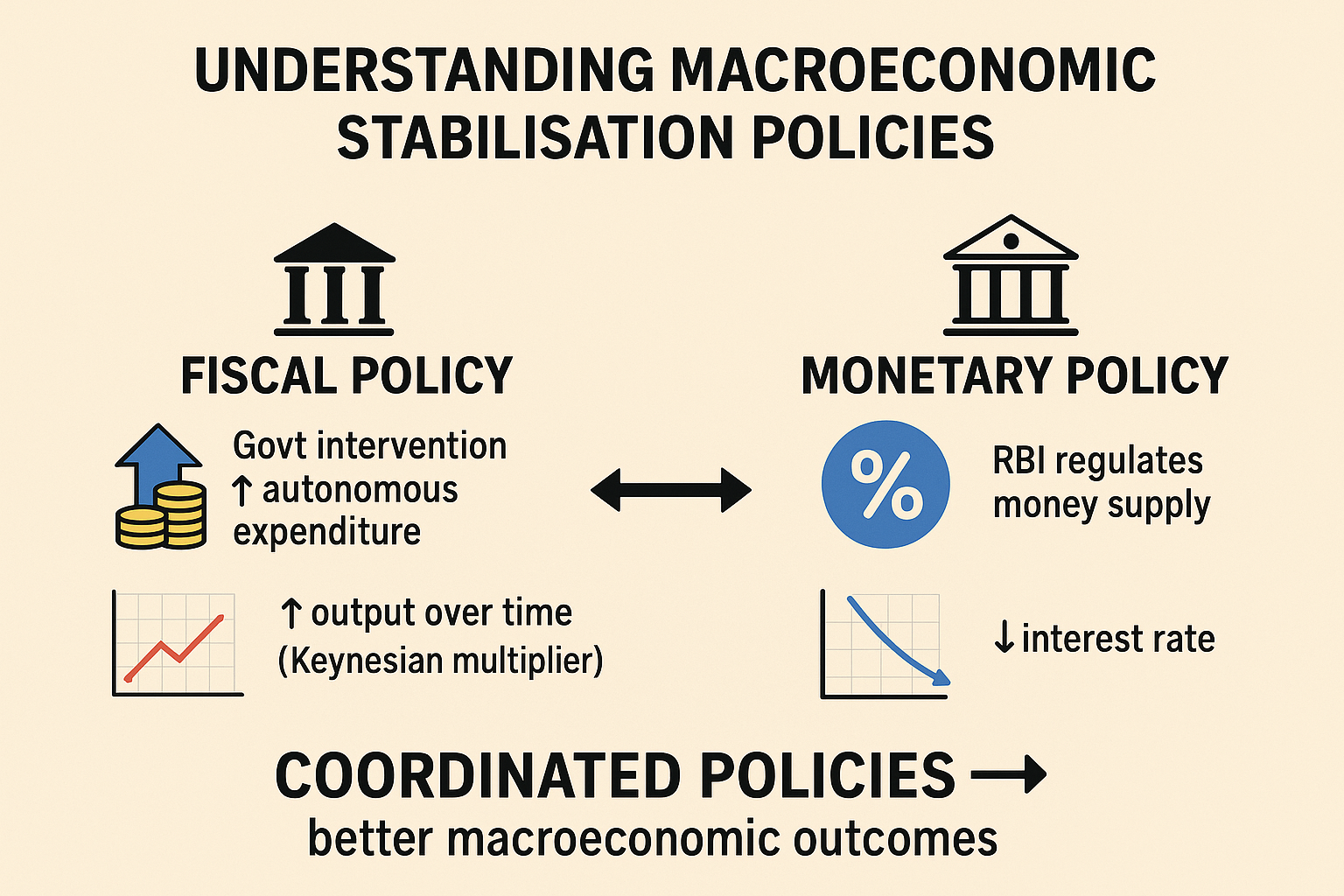

Two remarkable features define Keynesian economics. First, Keynes argued that to pull an economy out of a deep recession, the government must intervene by increasing autonomous government expenditure. Second, and more importantly, he demonstrated that national output would rise not merely by the amount of government spending, but by multiple times that amount. This phenomenon is known as the Keynesian multiplier. Nations aspire to achieve a sufficiently large multiplier so that government spending can meaningfully boost output and employment.

These ideas triggered what is often referred to as the Keynesian Revolution, and were adopted by governments across the world. As the French saying goes, “Laissez-faire ended when the state had to save the market.”

In India, fiscal policy is articulated primarily through the Union Budget, presented by the Finance Minister, which outlines the government’s revenue and expenditure priorities. Over the years, the Prime Minister and the government have also shaped fiscal policy through reforms, amendments, and targeted spending programmes.

However, fiscal policy is not without unintended consequences. Increased government spending often leads to a rise in interest rates, as the government competes with the private sector for available funds. This raises borrowing costs for businesses and households, reducing private investment and consumption a phenomenon known as crowding out.

This is where monetary policy plays a complementary role. Monetary policy is conducted by the Reserve Bank of India (RBI) through its Governor and the Monetary Policy Committee (MPC). The RBI’s primary mandate is to maintain price stability, with an inflation target of 4 per cent, allowing a tolerance band of ±2 per cent. Using instruments such as changes in the Cash Reserve Ratio (CRR), policy interest rates, and open market operations (buying and selling government securities), the RBI regulates money supply and liquidity in the economy.

If fiscal expansion leads to higher interest rates, the RBI can offset this by increasing money supply, thereby easing interest rates and supporting investment. In this way, effective coordination between fiscal and monetary policy can produce better macroeconomic outcomes.

As a seasoned civil servant and former Revenue Secretary, the RBI Governor is well-positioned to understand the fiscal constraints and growth priorities of the government. Such institutional coordination strengthens macroeconomic stability and enhances the effectiveness of policy interventions.

In macroeconomic management, it truly takes two to tango fiscal and monetary policies working in harmony to stabilise growth, control inflation, and sustain long-term development.